COMMUNICATION TO EMPLOYEES OF HARMERS WORKPLACE LAWYERS REGARDING MYSUPER – NOVEMBER 2013

Employees of Harmers Workplace Lawyers – MySuper

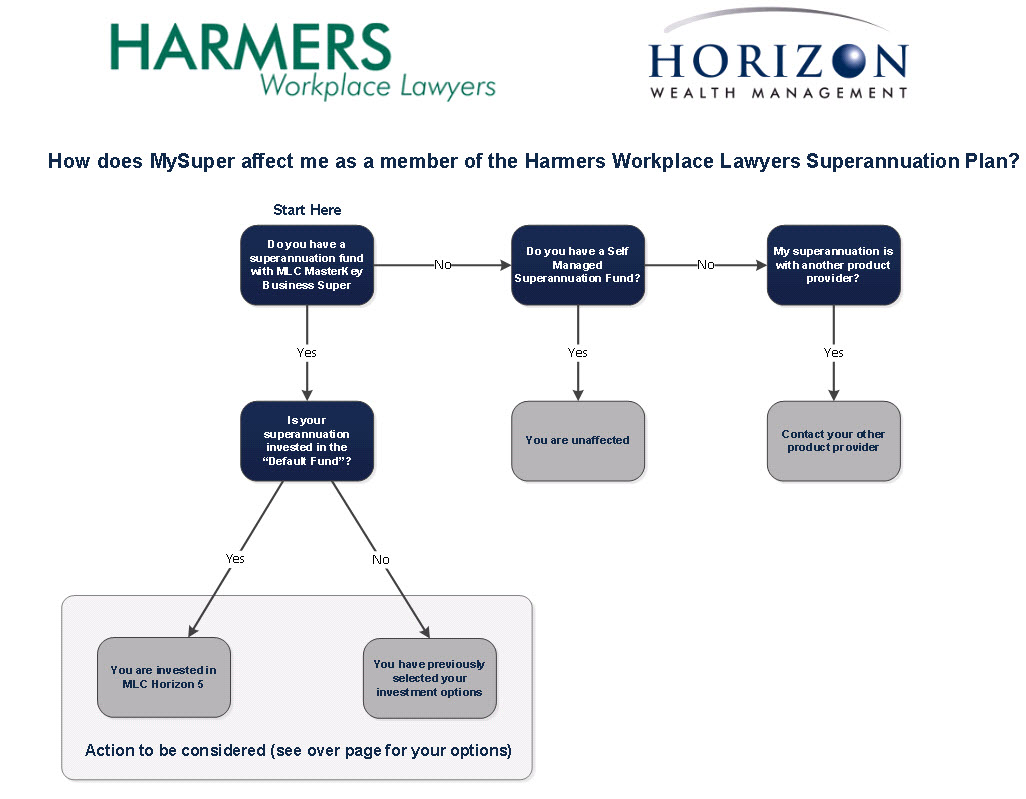

The recently enacted MySuper legislation has the effect of creating a new MLC MasterKey Buisness Super (MLC) Plan Default Fund which will impact employees who are a member of the current Harmers Workplace Lawyers Superannuation Plan AND who have not selected their own investment option/s.

Employees who are not a member of the Harmers Workplace Lawyers Superannuation Plan through MLC AND who have directed superannuation contributions to a Self Managed Superannuation Fund (SMSF) will be unaffected and can ignore this communication.

Employees who are not a member of the Harmers Workplace Lawyers Superannuation Plan through MLC, AND who currently have employer superannuation contributions directed to an alternative Product Provider should contact that Product Provider in order to establish what actions may be required to be taken. This note is not relevant to your circumstances.

MLC MasterKey Buisness Super are launching their MySuper Superannuation investment option on 29 November 2013 as part of their existing product. All future employer superannuation contributions post 29 November 2013 will be affected and therefore your consideration of the issues summarized below is required.

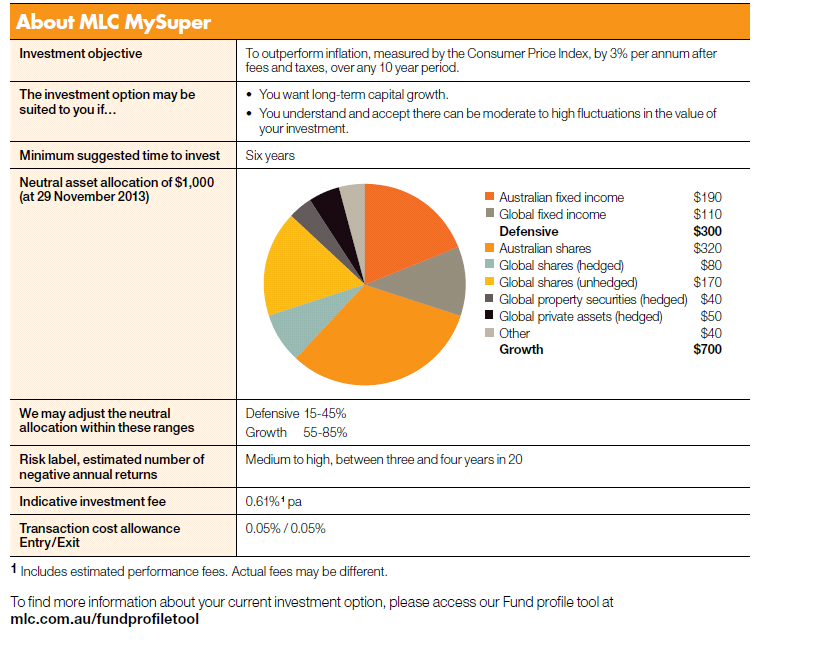

MLC’s MySuper investment option has a Growth bias with approximately 70% invested in Growth Assets and 30% in Defensive Assets (the neutral asset allocation). The asset allocation can move as follows

- Growth from 55% to 85%

- Defensive from 15% to 45%

This will become the new Default Plan option with effect from 29 November 2013.

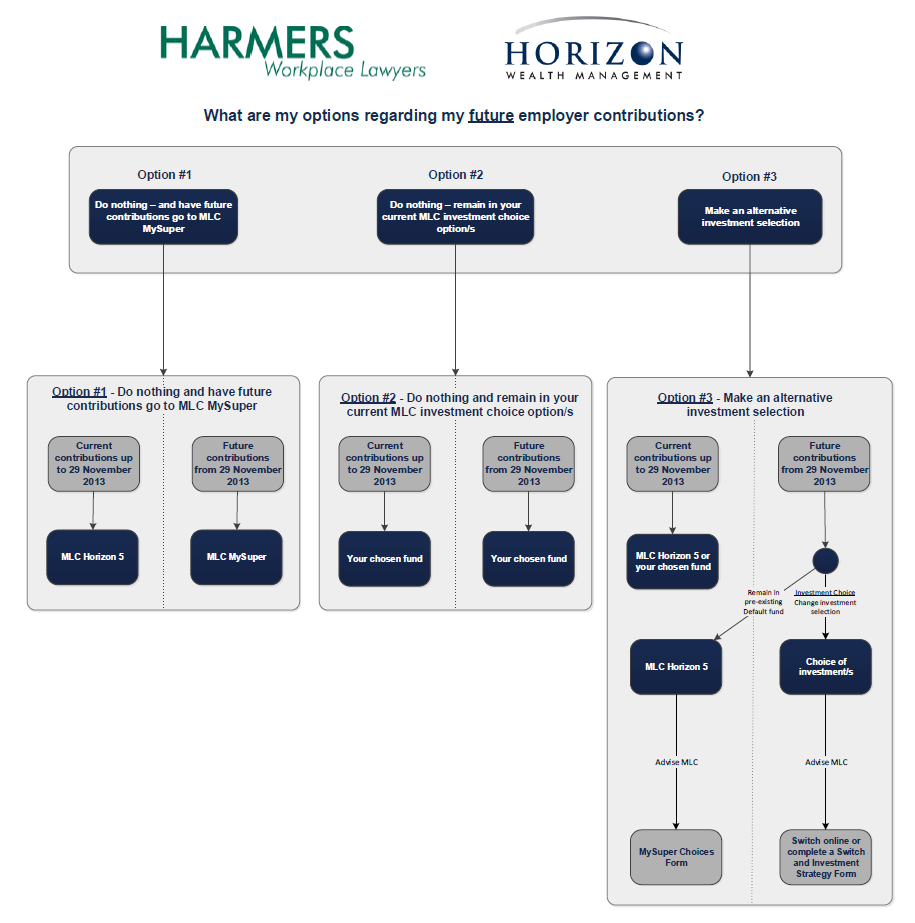

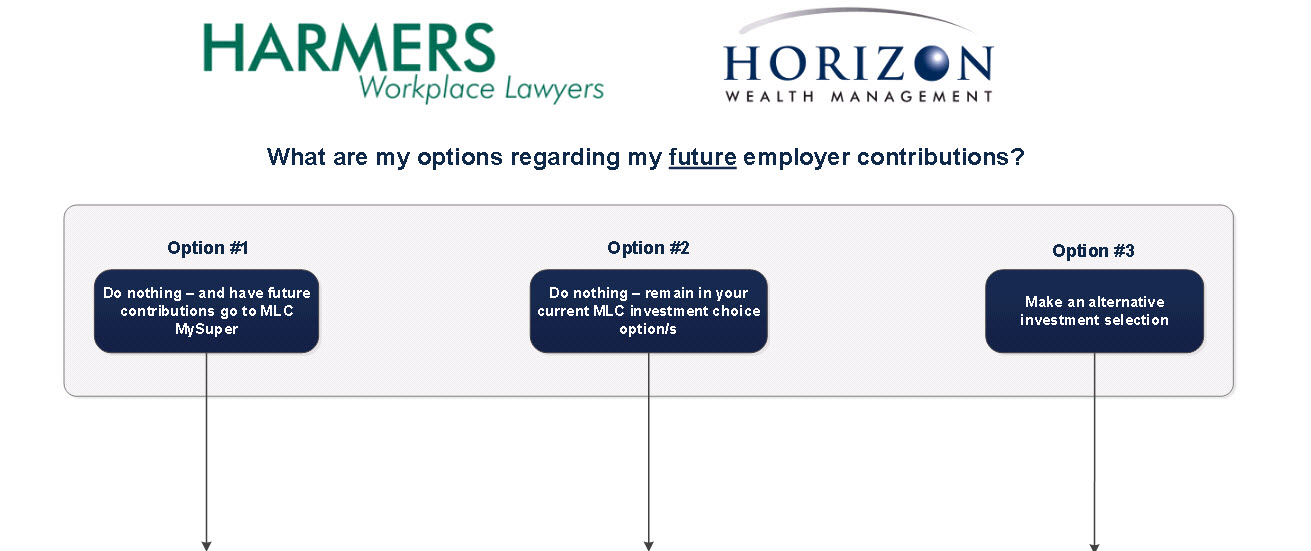

What are my options in respect of your future contributions?

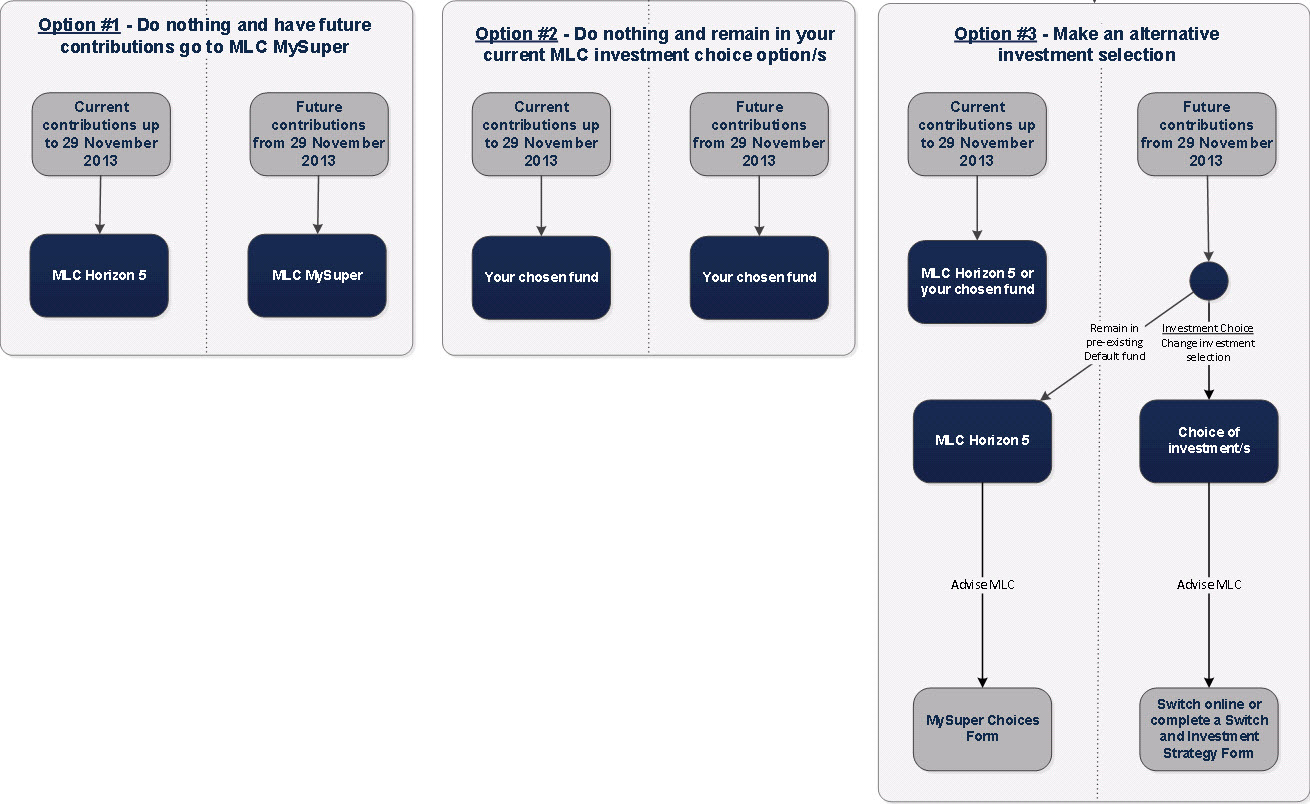

- Option 1 – Do nothing and have future contributions go to MLC MySuper.

- Option 2 – Do nothing and remain in your current MLC investment choice option/s.

- Option 3 – Make an alternative investment selection.

To view an enlarged version of this flowchart in a new window please click here.

Option 1 – Do nothing and remain in the Plan Default investment option

If you have never elected an Investment Option, your current contributions are being directed into the current Default option, being MLC Horizon 5. All future contributions from 29 November 2013 will automatically be paid to the new MLC MySuper Default option noted above.

Option 2 – Do nothing and remain in your chosen MLC investment option

If you have a current MLC Investment choice option/s other than the Default investment option, all future contributions will be paid to the same fund. You should refer to the MLC correspondence you have received to determine the specific costs related to your particular investments.

Option 3 – Make an alternative investment selection in respect of your future contributions

After 29 November 2013, you may wish to continue to direct your future contributions to the MLC Horizon 5 Fund, or change your current MLC investment selection.

In this case the existing fee scale of 1.56% will apply for future contributions to MLC Horizon 5. Please note that if your balance is greater than $50,000, then the account keeping (Member) fee of $1.50 per week will be waived.

If you wish to retain your Horizon 5 fund for future contributions, you will need to complete the MySuper Choices Form prior to the 7 November 2013.

If you wish to to change to an alternate option, you can do so online or by completing a ‘Switch and Investment Strategy Form’.

What are my options in respect of the current balance in my superannuation fund?

Please note: If you are currently invested in the Default option (MLC Horizon 5), your future contributions will be invested in the MLC MySuper Default option noted above. You will therefore have funds in both MLC Horizon 5 AND the MLC MySuper Default option. Should you wish to combine both fund balances into your new investment selection, you will need to complete a a ‘Switch and Investment Strategy Form’ or do a switch online.

Open flowchart diagrams in new window HERE.

Comparison of costs associated with the:

- Current Default Fund (MLC Horizon 5) – up to 29 November 2013

- New (MLC MySuper) Default fund – post 29 November 2013, and

- Costs of MLC Horizon 5 – post 29 November 2013

In the table below:

- The first column relates to the costs in respect to your current balance pre 29 November 2013.

- The 2nd column is the new default option post 29 November 2013.

- The 3rd column relates to the costs applicable to contributions post 29 November 2013 (should you wish to remain in the same default investment option in which you are currently invested).

|

|

Pre 29 November 2013 |

Post 29 November 2013 |

|

|

|

|

MLC MySuper |

|

|

MLC Horizon 5 |

(New Default) |

MLC Horizon 5 |

|

|

Total retail MER |

1.56% |

1.01% |

1.56% |

|

Member Fee |

$78 per annum* |

$78 per annum |

$78 per annum* |

* Please note that if your balance is greater than $50,000, then the account keeping (Member) fee of $1.50 per week will be waived.

Comments on Asset Allocation:

- The current default fund, MLC Horizon 5, the asset allocation is 85% Growth and 15% Defensive.

- The asset allocation of the new default fund, MLC MySuper will initially be 70% Growth and 30% Defensive.

Asset allocation is a key consideration in fund selection and is dependent on your personal risk profile and risk appetite.

What happens if I am not a current member of MLC MasterKey Business Super and wish to join?

If you are an existing employee, you are required to complete a Superannuation Choice Form available from Renee. All new contributions after 29 November 2013 will then be directed into the new default fund.

Please feel free to call Brian or myself if you have any questions, concerns or suggestions at anytime.

Brian May

phone: +61 2 9392 8700

email: brianm@horizonwealth.com.au

Kind regards

Renee Gase-Patterson

General Advice Disclaimer

This document is not meant to replace or contradict the PDS (Product Disclosure Statement). You are advised to read the PDS should you wish to obtain the full meaning of any terms or benefits noted above.

This information was prepared by Horizon Wealth Management. It is of a general nature and does not take into account your personal investment objectives, financial situation or particular needs. You should assess whether this general advice is appropriate to your individual objectives, financial situation and needs. You can make this assessment yourself or seek the help of a professional financial advisor or taxation professional.