It’s around this time of the year that all superannuation funds report their performances and it can be challenging to sensibly interpret this information; including how it compares with your own fund performance.

Labels can be confusing, so terms like Balanced and Growth can be interpreted differently. It’s far better to use precise language where ‘apples can be compared with apples’.

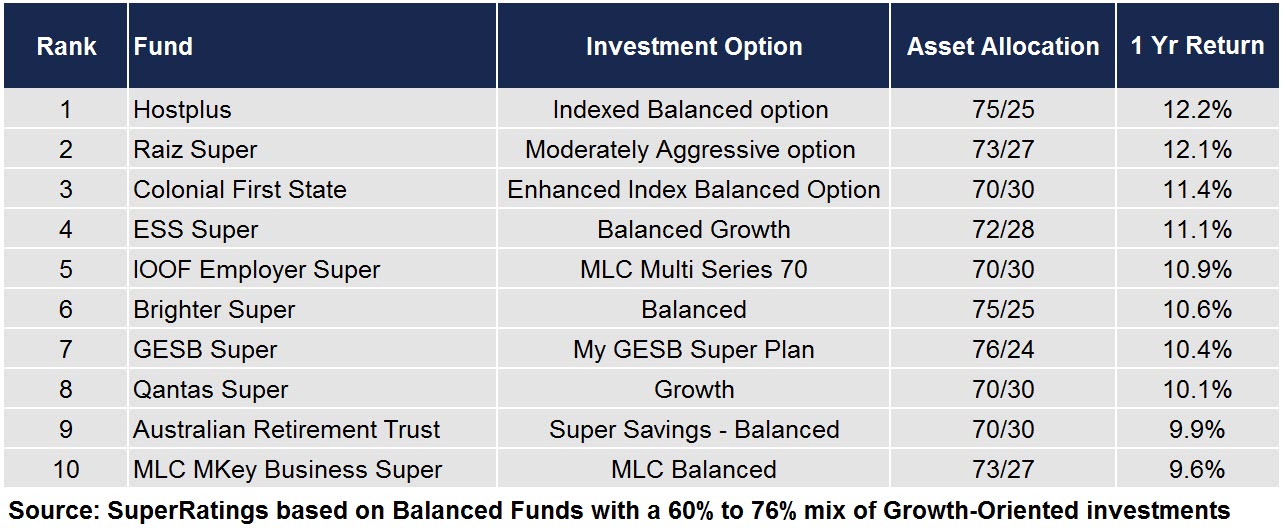

Below are the top 10 best performing funds for One Year, in the year to 30 June 2024. These funds were all in the category with 60% to 76% in Growth-Oriented investments, and the remainder in Defensive investments.

Table 1

There are some industry super funds that tend to classify 50% of their Property and Infrastructure exposure as Defensive (rather than 100% as Growth assets) as we typically would disclose these asset classes.

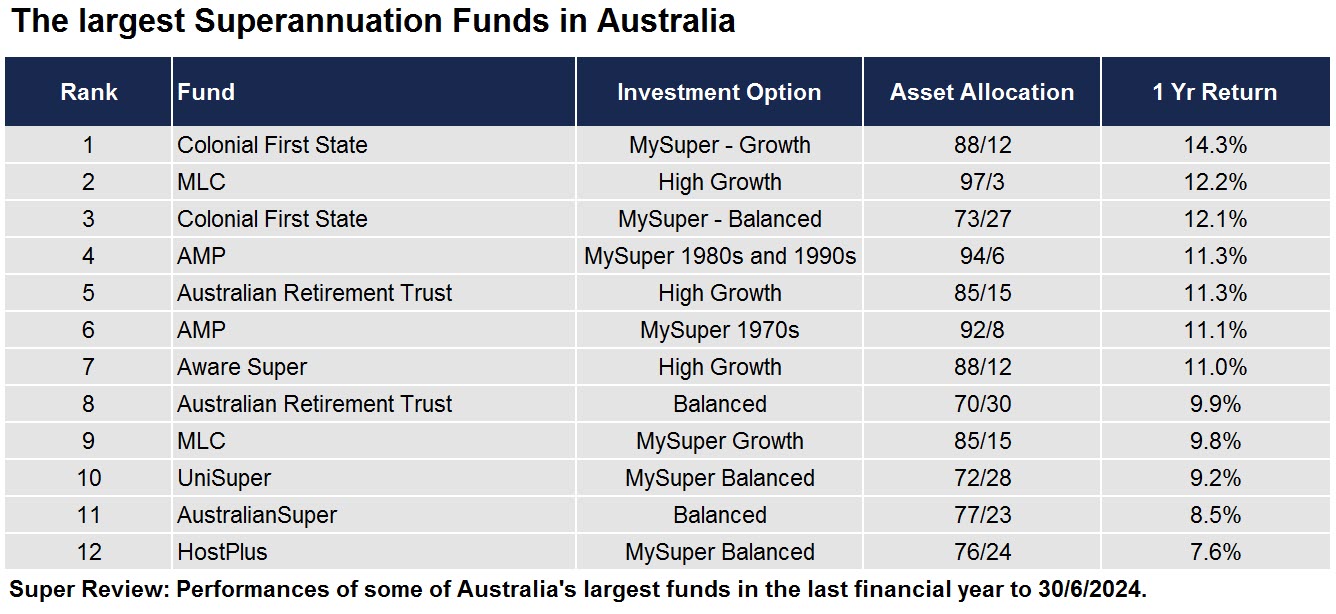

How did some of the largest funds in Australia perform?

Bear in mind that the asset allocation of the superannuation funds in Table 2 below varies significantly from Table 1 above. In other words, during the 2024 financial year, the higher the level of Growth Assets in the portfolio, the higher generally was the performance.

Table 2

So how did AustralianSuper do as an example?

‘The country’s largest fund, AustralianSuper, reported a “solid” return of 8.46% from its Balanced option for the financial year 2023/2024, bolstered by strong performances from share markets. While the $335 billion fund slightly lagged some of its mega fund counterparts, Mark Delaney, AustralianSuper chief investment officer, said it was a “pleasing” result all round, particularly as the fund was more defensively positioned up until December 2023’.

So how do these returns compare to our Client’s Portfolios?

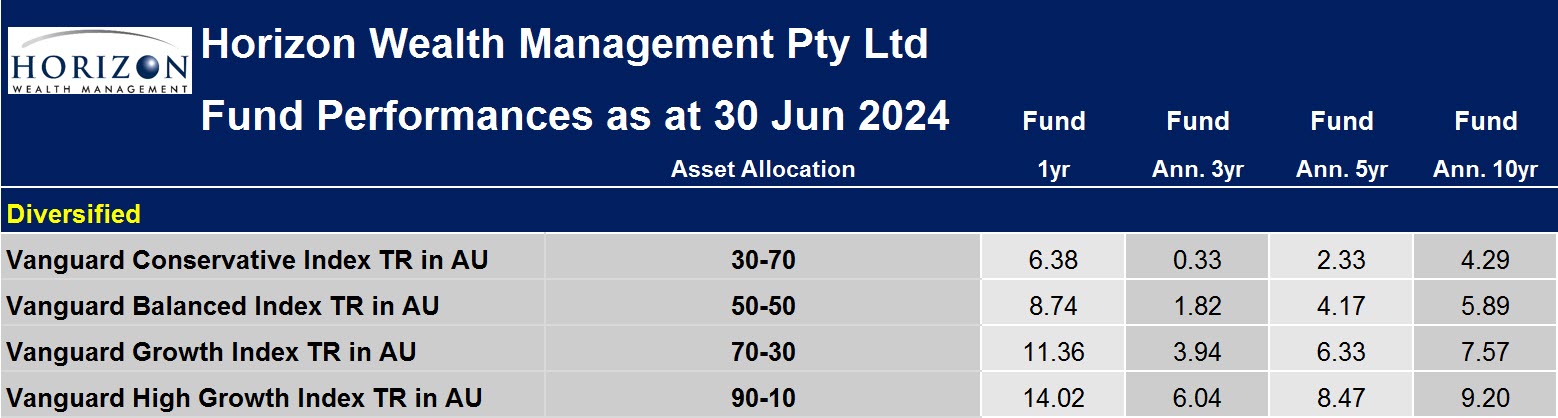

First, it’s worth reviewing the diversified range of the Vanguard funds which we use for certain client’s circumstances, as well as benchmark to our returns.

For the purpose of this comparison, Vanguard use the term Balanced to describe a 50/50 (Growth/Defensive) Investment option so you can see how confusing labels (without a proper explanation) can be. We choose to avoid this ambiguity by disclosing the actual asset allocation of each fund.

If one looks at the Vanguard Growth Fund and Vanguard High Growth Fund in Table 3 below, whose asset allocations are 70/30 (Growth/Defensive) and 90/10 (Growth/Defensive) respectively – one can see that either the average of the asset allocation of both the Growth Fund and the High Growth Fund or just the High Growth Fund on its own, correlates closely to a number of the ‘top funds’ asset allocations in Table 2 above. In this case, the performance of the Vanguard Growth Fund compares favourably at 11.36% for the one-year return to 30 June 2024. It should be noted that superannuation tax should be applied to these Vanguard returns to again compare ‘apples vs apples’. If one assumes an earnings rate of 3% and a superannuation tax rate of 15%, it would be appropriate to reduce these returns by approximately 0.5%. Further, one could also reduce these returns further by an estimated administration fee of approximately 0.5%.

If we adjusted the Vanguard Growth Fund return of 11.36%, to be net of super earnings tax of 0.5% and administration fees of 0.5%, that would equate to 10.36% – and if we further reduced this by 1.1% as an estimate of the maximum of our advice fee that would reduce the return to 9.26%.

If we applied the same logic to the one-year return of 14.02% for the Vanguard High Growth Fund, the net return after all fees and superannuation tax would be an outstanding 11.92%.

Table 3

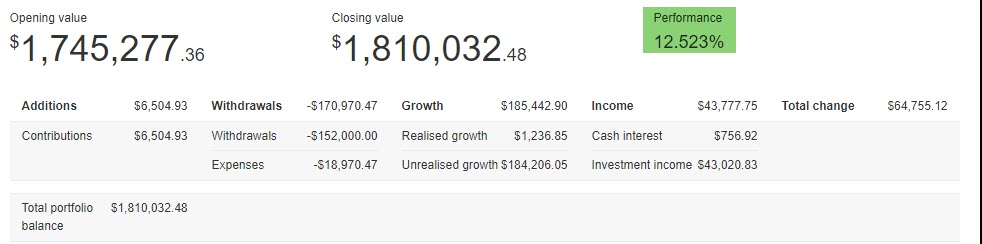

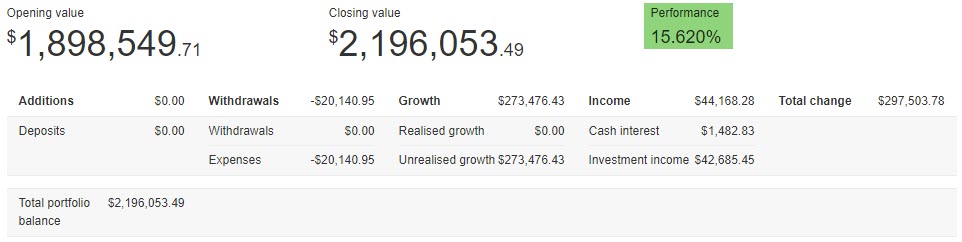

As a means of illustration, we have included 1 of our clients’ actual performance over the past 12 months to the 30 June 2024, whose portfolio was invested on a 70/30 basis and therefore comparable to Table 1 above.

It should be noted that our returns are calculated on a money weighted basis which is the most accurate method of calculating performances as it measures the timing of each cash flow whether it’s an inflow or an outflow.

These returns are net of both superannuation tax and net of all fees including our advice fees.

In the example below, there was also cash outflows on the portfolio and still an impressive 12.5% return after all fees (including our advice fee) and taxes.

Portfolio between 60% and 76% Growth Oriented Assets

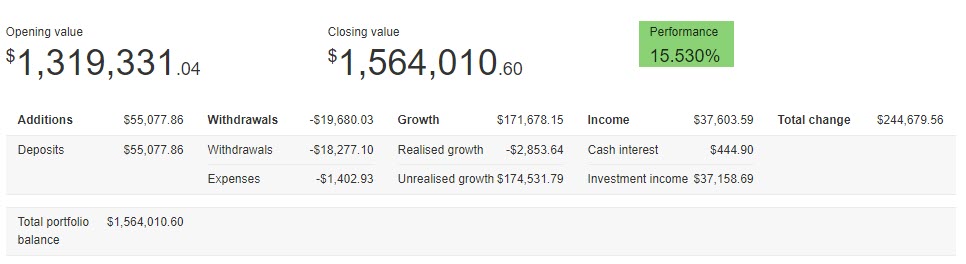

Portfolios with Growth Oriented Assets greater than 76%

The performances below are for clients that had a higher asset allocation than 76/24 (Growth/Defensive) and are therefore comparable to the largest funds in Australia per Table 2 above.

Reflection

The purpose of this note isn’t just to highlight and demonstrate that our performances were at the very least on par with those of the best performing funds, but more to explain some of this meaningless terminology noted in the press without context.

There is no doubt that our clients’ portfolios in general have benefited from:

- Being significantly overweight International Equities relative to Australian Equities.

- Having an unhedged currency position for International Equities.

- Being overweight US Equities with a bias towards technology.

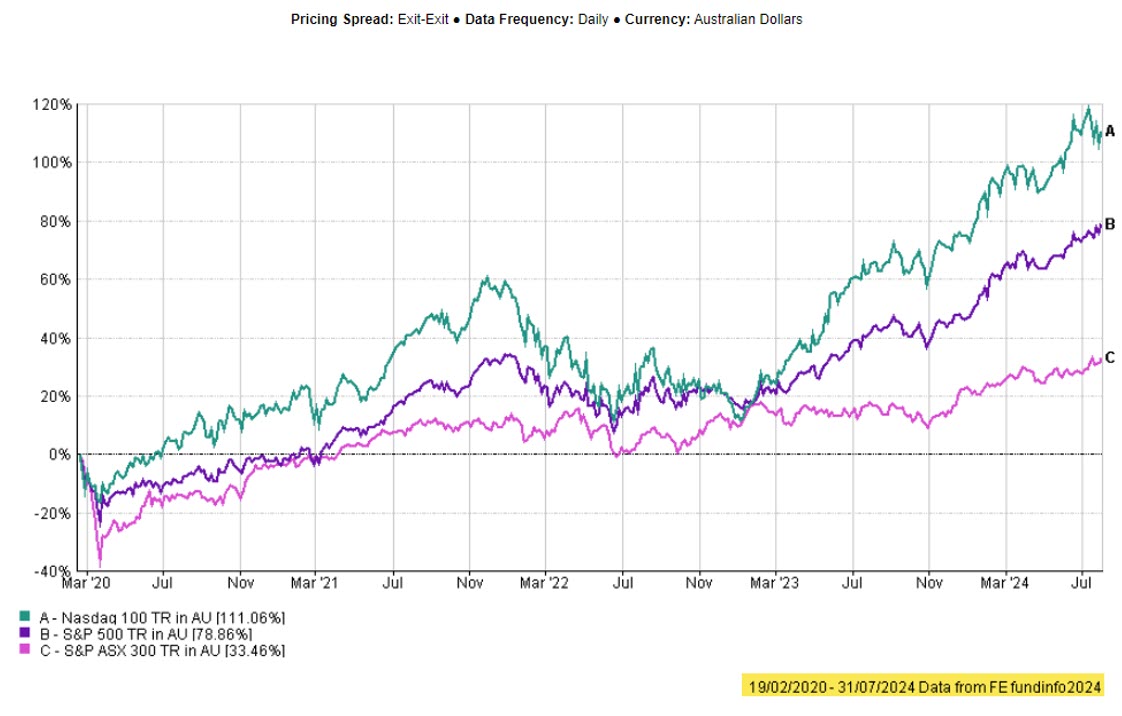

Table 4 below illustrates what a roller-coaster ride the last 4 years has been since Covid. Below are cumulative returns to 31 July 2024. The 1st and 3rd column represent the highest points in the cycle at that time. The main take out from this table is that:

- There are no negative returns, and

- If a crisis happens, it’s best to stay invested and ride it out.

Table 4

In Conclusion

Investing isn’t a sprint, but rather a marathon. Our goal is to provide counsel, advice and coaching to our clients whose financial success requires the specific expertise we have. We are privately owned and therefore have no pressure to sell or recommend solutions which may not be in your best interests.

Please note:

- This communication has been prepared for the purpose of providing general information, without taking any account of your objectives, financial situation or needs.

- You should – before making any investment-related decisions – consider the appropriateness of the information in this document, and seek our specific advice – having regard to your own objectives, financial situation and needs.