Have central banks been able to achieve something truly remarkable — a steady decline in inflation without further interest rate increases, and without bringing on a recession? Or are bond yields now doing the job for them? Yields continue to rise in the face of risks that include the conflict in the Middle East, rising oil prices, farce on Capito Hill in the US and sticky inflation. We may be close to the Terminal Rate for interest rates, but higher bond yields and geo-politics could still end up breaking something.

Introduction

Back at the end of 2021 the first signs that inflation was rising were becoming apparent, as global supply chains battled to keep up with demand in a post-Covid world. Originally Central Banks reassured markets that inflation was “transitory” and would soon pass. But after the Russian invasion of Ukraine in February 2022 energy and food prices soared, and Central Banks had to step in to combat inflation with the only tool they have – to raise official cash rates.

Inflation and how central banks react to it – and how the market reacts to the words and actions of the central banks – has been a central theme since the Federal Open Market Committee – “the Fed” – first increased the Fed Funds rate to a target of 0.25% – 0.50% back in March last year. Here in Australia the Reserve Bank followed soon after by lifting the official cash rate from 0.1% to 0.35% on May 4th.

Since then, the market has been continually coming to terms with expectations on how high interest rates will go before the central banks are done with this round of tightening – in other words, the market is trying to determine the “Terminal Rate” of interest rates, and what effects that will have on the economy and financial markets.

Expectations are Everything.

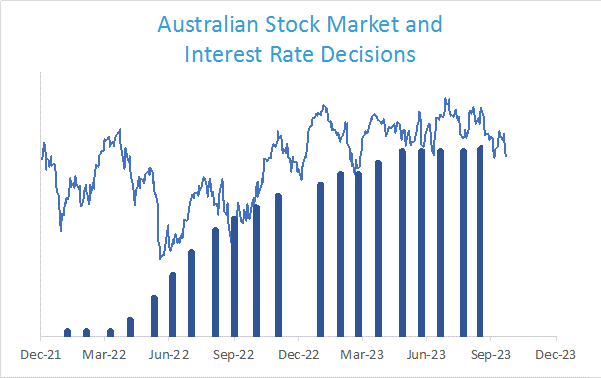

As shown in the chart below, the Australian stock market has been volatile over the last 2 years. It seems to be an on-going pattern of hope and disappointment as markets rally for long periods, but then fall back as they re-set their expectations on where interest rates would finish up and the consequences for company earnings and the economy in general.

ASX200 data from investing.com. Australian cash rate data from RBA.

While the media often suggests that RBA decisions are a surprise, in fact there is little correlation between the actual RBA decision and how the market reacts to it. For example, the S&P/ASX 200 started 2022 with steep falls in January – but this was on the expectation that rates would need to rise, rather than any actual rate increase.

By the end of 2022 inflation around the world had peaked and was coming back down. Consequently, stocks have rallied for most of this year driven by the equity market’s belief that the “terminal rate” for this cycle of interest rates is very close, and that the central banks would start cutting rates by the end of this year.

More recently, the RBA has deemed to keep rates on hold at 4.1% for the last 4 meetings – indicating that the “terminal rate” is indeed close, if not quite there. Yet markets have been coming off their highs since the end of July. If rate rises are on hold, then what is the cause of this renewed bout of negative market sentiment?

Why is the stock market falling if rates are on hold?

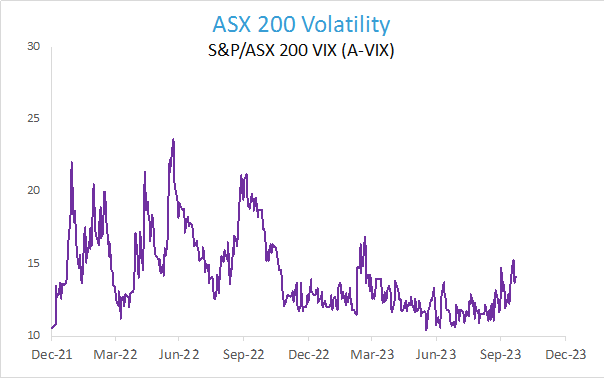

The Australian stock market is down around -6% since the end of July, and market volatility is now creeping back up. The chart below shows the volatility index – what some call the “fear gauge” – rising the most since the US banking crisis back in March, when there were concerns that the collapse of several US regional banks and Credit Suisse would have a contagion effect on the global banking system.

S&P/ASX 200 VIX data from investing.com

There are several reasons for this increase in volatility and corresponding correction in stock prices.

- Interest Rates will Stay “Higher For Longer.”

Firstly, central bankers around the world have emphasized that rates will remain “higher for longer”. If investors anticipate higher rates in the future, it reduces the present value of future earnings for stocks. The message is now coming in loud and clear that the central banks are not planning on a rapid policy pivot as many were expecting. While inflation is coming down, it’s not coming down fast enough due to strong labour markets and a resilient economy.

- Longer Bond Yields are Continuing to Rise

Secondly, bond yields continue to rise, which is having a greater effect on the economy than just the performance of bond funds. The US 10 year Treasury yield is the price of money for the world. This foundation for global markets has soared 90bps since the start of September alone – and in the bond world that is a big number. Much of global borrowings from corporates to households to emerging market sovereign debt is linked to longer term US yields.

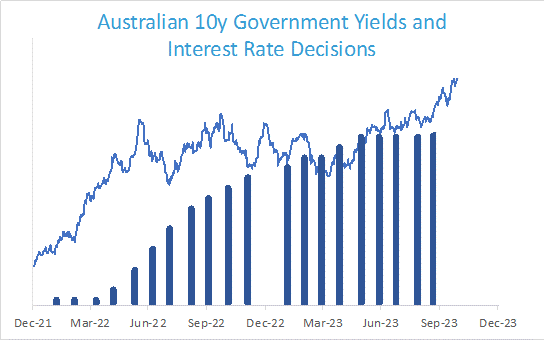

The Australian Government 10 year yield is closely correlated to its US counterpart and is now at levels not seen since 2011. The chart below shows the sudden rise in Australian 10 year yields even though official rates are on hold. Consequently, the interest rates on mortgages, credit cards and business loans have shot up in recent months, The rapid rise has startled investors and put policymakers in a tough spot – do they risk another rate rise to bring inflation down when the bond market appears to be doing the job for them?

Australian Government 10 year yield data from investing.com. Australian cash rate data from RBA

There are many reasons why natural buyers of US Treasuries are withdrawing from the market (forcing bond prices down and yields to rise), including uncertainty at how the current US political system will be able to defuse the ticking time bomb that is the US budget deficit. There is a limit to how much debt any government can accumulate before a debt spiral begins in which debt holders’ fear of default causes them to demand higher interest rates, which then causes higher deficits and more debt and then even-higher interest rates, deficits and debt in turn.

- Geo-Political Tensions are Rising.

And there is a third reason that market volatility is increasing – the conflict in the Middle East. The Israel-Hamas war is creating a heightened sense of market risk, which so far as hasn’t provoked the usual safe-haven flows in US Treasuries — although gold is up since the conflict began.

An escalation of the Israel-Gaza war into a broader conflict – potentially one involving the United States and Iran – could deliver another shock to world growth and halt disinflationary forces in their tracks. A broader conflict could send oil prices soaring and damage a global economy already straining under higher interest rates.

As well, the conflict in the Ukraine continues, which also effects oil and food supplies, both of which are contributors to global inflation. And tensions between China and the U.S. continue to run high — leaving American companies having to carefully navigate their approach to a key player in the global economy, particularly around technology.

Are we at the “terminal rate” – or are there more rate rises to come?

The aggressive monetary tightening of the last 18 months is only now filtering through to the economy, complicating assessments of whether the RBA has done enough to rein in prices and get inflation back to its target band. The latest Australian Consumer Price Index data (released on 25 October) shows inflation rose 1.2% in the September quarter so the case for further rate hikes remains strong.

The latest RBA Minutes have reiterated that “Whether or not a further increase in interest rates is required would, therefore, depend on the incoming data and how these alter the economic outlook and the evolving assessment of risks.”

The emergence of several unexpected headwinds such as the conflict in the Middle East, higher bond yields, rising oil prices, political farce on Capitol Hill and sticky inflation are all contributing to continually changing expectations around growth. Economies and markets are going through a transition from zero rates back to more normalised levels with these transitions taking time and accompanied by elevated uncertainty and volatility.

However, investors should remain optimistic despite the prospect of slowing economic growth. Markets are forward looking and price in their expectations around future growth immediately, whereas economic data is backward looking. The recent correction in the market may have priced in the current risks to the economy whether there are further increases in rates or not. As we come to the end of 2023 we may see equities continue their long term path of rising, while bonds now offer higher income and the ability to protect a diversified portfolio.

Source: Dr Steve Garth

Principia investment Consultants and member of Horizon Wealth’s Investment Committee