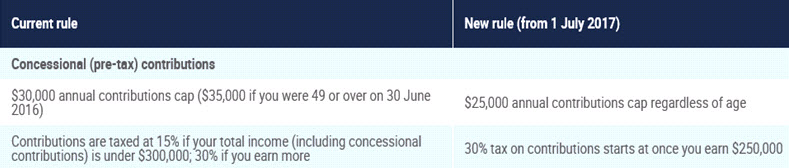

Concessional contributions

Changes to the annual concessional contributions cap, and the income threshold at which a 30% tax rate will be applied to your concessional contributions follow:

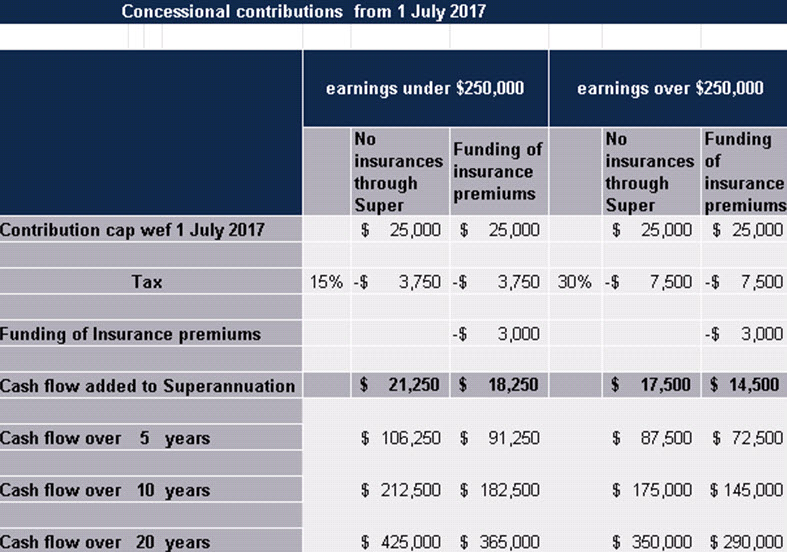

We have laid out the potential impact of the changes over time in the table below.

On the left hand side we assume your earnings are less than $250,000, and on the right hand side we assume your earnings are greater than $250,000.

We have also assumed in each of the 2 situations above that you may or may not fund insurance premiums through your superannuation.

On the basis you:

- can afford to make the full $25,000 annual concessional contribution*,

- earn over $250,000 pa*, and

- utilise your superannuation account to fund a small portion of your insurances*.

* in this scenario above you would add $290,000 in cash flow to your superannuation balance – over a 20 year period – refer table above.

It is evident that these changes are going to reduce one’s capacity to build up material super balances over the next 5 to 20 years.

Unless you:

- have a major inheritance coming, or

- have a significant passive asset that you are planning to dispose of in the next few years, or

- own a business or shares in a business that you intend selling.

It will be impossible to build up substantial assets inside superannuation to fund your retirement through concessional contributions in isolation.

More about that in the next article on non concessional contributions.